Queensland has updated the Capacity Assessment Guidelines which are to be applied in assessing an adult’s capacity to make decisions. The Guidelines assists practitioners, families and the public in testing the key criteria of capacity. The following summarises the critical sections of the Guidelines.

What is capacity?

Capacity is a legal term referring to the ability to exercise the decision-making process.

When an adult has capacity to make a certain decision, they are able to:

» understand and retain (even for a short while) the information relating to the decision

» understand the main choices available

» understand and weigh up the consequences of the choices

» communicate the decision

» make a decision freely and voluntarily.

It is the adult’s ability to exercise the decision-making process that is assessed when you carry out a capacity assessment.

It is important to remember that while an intellectual or cognitive impairment might impact on an

adult’s decision-making ability, it doesn’t necessarily mean they lack capacity. The same can be said

for mental illness, brain injury, dementia and age. Whether the adult makes a decision that others

might think is wrong, risky or immoral is also irrelevant.

The five principals in assessment of capacity:

Always presume an adult has capacity: Under the law it is not up to the adult in question to prove they have capacity. It is presumed that every adult has capacity to make all decisions until proven otherwise. This presumption is not affected by any personal characteristics such as disability, mental illness or age (if the person is over 18 years of age). The responsibility is on the person seeking to challenge the adult’s decision-making capacity to prove the adult has impaired capacity. This can be done through a capacity assessment.

Capacity is decision-specific and time-specific: Capacity is specific to the type of decision to be made and the time the decision is made. Someone might have capacity to make certain types of decisions (e.g. a personal decision about where to live) and not others (e.g. a financial decision about whether to sell their house).

Provide the adult with the support and information they need to make and communicate decisions:

Capacity can fluctuate: Capacity can change or fluctuate. An adult with a medical condition or illness may temporarily lose capacity, but then regain capacity at a later date. On the other hand, an adult with dementia or delirium, for example, might have capacity on some days (or during some parts of the day)and not others.

Capacity can change with support: An adult’s capacity can improve depending on the support available to them. For this reason, an adult cannot be found to lack capacity until all practical steps have been taken to provide the support and information needed to make the decision.

Assess the adult’s decision-making ability rather than the decision they make: An adult is free to make bad or poor decisions, provided they have the decision-making ability to make that decision. It is not the decision that is tested, but the capacity to make any decision.

Respect the adult’s dignity and privacy: This process is perhaps the most invasive and overwhelming in the adult’s life. At all times, the adult is to be given dignity and privacy in the process and given full advantage of assistance to ensure that the adult’s decision-making capacity is truly impaired. Planning the capacity ahead of time and performing the assessment in circumstances comfortable to the adult are critical.

Tests of Capacity:

General test of capacity —is applied when assessing capacity for decisions about personal,

health or financial matters. This test requires the adult to:

understand the nature and effect of decisions about the matter;

freely and voluntarily make decisions about the matter; and

communicate the decision in some way.

Test for making an enduring document—is applied when assessing capacity for making an

advance health directive or enduring power of attorney. This test requires the adult to:

understand the nature and effect of the document. The law requires the adult to actually understand the powers the document gives and when it operates and how and when it can be cancelled or revoked; and

make the document freely and voluntarily.

Our practitioners are frequently called to assist families in both the making of estate planning documents, and in effecting processes once loved ones lose capacity or there is a question of a loss of capacity. We are compassionate and understanding, and can assist in a wide range of services when this time comes.

If you or your family has a concern about capacity or wishes to make estate planning instruments, please do not hesitate to contact our scheduling director, Vicki Baker, on 61 7 5574 3560 or Vicki@nautiluslaw.com.au to arrange a meeting. We conduct meetings by Zoom or in person.

Thank you – Katrina Elizabeth Brown, Senior Lawyer (Katrina@nautiluslaw.com.au)

In the matter of Calvin & McTier [2017] FamCAFC 125 (12 July 2017), the Full Court heard an appeal by a husband who argued that an inheritance received FOUR years after separation should not be included in the property to be divided. The Full Court held that the property to be divided in a matrimonial matter is the property held by the parties at the date of HEARING, not date of SEPARATION.

The husband’s counsel submitted a number of legal arguments to defeat the inclusion of the inheritance, including the proposition that if the inheritance was to be counted – the later acquired inheritance should be subject to a separate finding as to division (in that case, the inheritance equated 32% of the property pool, which the trial court awarded 65% to husband, and 35% to wife). The Full Court did not agree. The Full Court determined that a trial court has discretion to make decisions as to the whole of the assets of the parties, including assets acquired long after separation. To make matters worse, the husband was left to pay the parties’ costs.

The lesson here is that if your beneficiaries are separated, but have not resolved matters by a binding financial agreement or court orders (far preferred because of the finality), then you should be revisiting your estate planning and contemplating proper testamentary trust structures with adequate appointor and guardian provisions.

Also, if you have separated, but believe the cost of making a binding financial agreement and/or seeking court orders is “too hard” or “not worth the expense”, think again. It is far better to divide what is your marital pool, than risk dividing what is your later accumulated wealth. Whilst adjustments and contribution weighting may allow for a factor which compensates for your later accumulated wealth, you most likely will lose part of that accumulated wealth.

Life is a gamble, sometimes you win the gamble.

If you aren’t up for the gamble, we welcome you to contact one of the estate planning and/or family lawyers at Nautilus Law Group. Please free to contact Katrina Brown on (07) 5574 3560 or by email.

An Enduring Power of Attorney appoints an “Attorney” to act on your behalf in relation to the administration of your affairs at a time of your choosing, including following your incapacity.

Such appointment can be made in relation to both financial and personal/health matters. Should no such document exists upon your incapacity, there are various courses of action that can be taken in relation to the appointment of persons to act for you.

Personal and Health Matters

Pursuant to section 63 of the Powers of Attorney Act 1998 (Qld) (the Act), your spouse (if the relationship is close and continuing) is considered as the statutory health attorney, and can make any decision about the health matter that the Principal could lawfully make if they had capacity (in accordance with section 62 of the Act).

In the event your spouse is unable or unwilling to act, the Act provides alternate appointments and an application can be made to the Queensland Civil and Administrative Tribunal (QCAT) for recognition of same.

Financial Matters

QCAT can appoint a person to act as a Guardian for a person only if they are satisfied that the adult for whom the Guardian is appointed (the Principal) has impaired decision making capacity and that a decision maker is needed to ensure the Principal’s needs are met and protected.

Anyone who has a genuine and continuing interest in the welfare of the Principal can apply for appointment as the Guardian for such person. This power is not necessarily automatically given to your spouse.

Although there are provisions by which a health and finance attorney can be appointed to act on your behalf, this can be a lengthy and costly process and, in the event of your incapacity, can add additional stress to those persons already concerns for your welfare.

Further, a document specifically prepared by you which appoints your preferred Attorneys can provide additional instructions to such Attorneys (which instructions, if the Court were to make, would require additional processes and orders – some of which simply may not be possible). For example, in the event that you required your Attorney to deal with jointly held property or to make a nomination (binding or non-binding) to your superannuation trustee in relation to the payment of your member interests. As such terms can be important to the smooth and effective administration of your Estate, it is important to consider the drafting of a detailed Power of Attorney.

If you would like to discuss the drafting of your Enduring Power of Attorney, please contact Vicki on 07 5574 3560 or via email to info@nautiluslaw.com.au.

You drafted a Will years ago – it’s pretty basic, but it gives everything to your spouse, or, if your spouse doesn’t survive, then everything goes to your children. So, if the content of the Will applies, what is the point of doing a new Will that sets out the same wishes?

Many people see the updating of a Will as an unnecessary and costly exercise, particularly when the new Will contains the same directions as the prior Will.

Although we certainly understand the frustration with the process, there are three important reasons to ensure your Will is reviewed and updated regularly.

Firstly – a regular review of your Will is critical

There have been recent cases in Queensland that indicate that if a challenge is made against the Estate of a deceased person, and the Estate is being administered by a Will that was not recently made or reviewed, the Courts often question whether the wishes of the deceased at their date of death were the same as those contained in the Will.

There is good reason for this. We regularly hear “I’ve been meaning to update my Will for months now, especially since this happened” – life is busy, and updating a Will falls a long way down the to-do list for most people.

However, it is important to make time for the review process – attending on your solicitor to review the Will, make any alterations, or confirm your wishes can clarify your intentions for the administration of your Estate and potentially prevent an Estate challenge. There is no defined review period, however we recommend reviewing your documents with your solicitor at least every three years.

Secondly – legislation and case law changes regularly – your documents need to change with it

Legislation and Case Law in each State is constantly evolving, meaning that the way your Will is interpreted or effected may change over time.

It is important to review, and confirm or vary, your Estate planning documents with your solicitor regularly to ensure that there are no material changes to your Estate plan that result from changes in law.

Finally – has your Will been voided or revoked?

While a regular review of your Estate planning documents is important, there are certain circumstances which will void your Will – therefore, review is critical should any such occasion occur.

Marriage, for example, will revoke a Will. Unless your Will is made in contemplation of your marriage to your partner, the act of marrying will invalidate the Will.

Similarly, divorce or annulment will also revoke your Will (unless a contrary intention is specifically indicated).

It is also important to review your Will as the circumstances of yourself, your executors or your beneficiaries change – if you, your executors or your beneficiaries become subject to bankruptcy or family law proceedings, it is important to review your Estate plan to ensure that it is still appropriate and, where necessary, that appropriate protective measures are set in place.

If you need to review your Estate plan, we welcome you to contact our Estate Planning Team on 07 5574 3560 or via email.

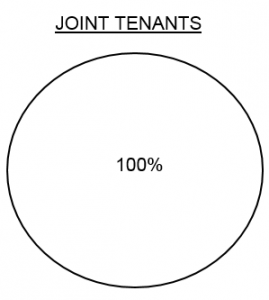

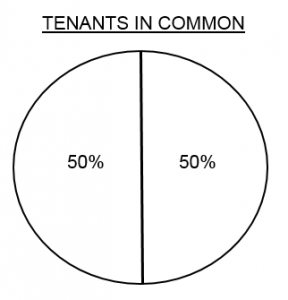

If you hold real property with another person, it is important to know whether you hold the property as joint tenants or as tenants in common.

What’s the difference?

A joint tenancy is where two (or more) people (or legal entities) own an asset jointly – that is 100% of the asset is held in ALL names. No one owner has a fixed interest in the asset. This is commonly the situation between spouses. When one owner of the asset dies, their death is recorded and the asset automatically transfers into the name of the surviving owner. A “jointly held” asset does not (except in some instances in New South Wales) pass to your estate – it passes to the survivor automatically.

Conversely, a tenancy in common is where two (or more) people (or legal entities) own an asset, but each person owns a specified share. This situation is common in business dealings and in dealings where parties wish to own distinct interests in an asset. The below diagram shows a “tenancy in common” between a husband and wife, with the husband owning 50% of the asset, and the wife owning 50% of the asset. On the death of one of the spouses, their share passes to their estate and is distributed in accordance with their Will. The share does not pass automatically to the surviving spouse.

There are benefits and downsides to each type of holding; accordingly, owners need to be aware of the consequences of each option – to ensure suitability.

What happens if I want to change the way the asset is held?

If you hold an asset as joint tenants, and wish to sever the tenancy, or if you hold the property as tenants in common in equal shares and want to become joint tenants, it is possible to change the way the property is held. These transactions are commonly effected for estate planning or family law purposes.

This change is effected by way of a form signed by one or both property owners, which is then stamped and registered with the Titles Registry as a change of tenure transaction. In some circumstances, there is a transfer duty exemption which can apply.

If you wish to discuss changing the tenure on your property, please contact our office on 07 5574 3560.

It is a common phrase heard, particularly from young adults – “I don’t have any assets, so I don’t need a Will”.

Young adults and non-homeowners are often of the opinion that, because they do not have “significant” assets – they do not need a Will. This article considers two of the most basic reasons to have a Will.

Firstly, everyone owns something – and the majority of young people have potentially significant superannuation death benefits.

Remember opening a “Dollarmites Club” account with Commonwealth Bank when you were in early primary school (or opening one for your children)? At a young age you started to accumulate assets.

In addition to many young adults concluding that their assets are not significant enough to necessitate a Will, there is generally one asset that they do not consider – superannuation death benefit proceeds.

Superannuation is held by the Trustee of your superannuation fund(s) on your behalf. Although you are beneficially entitled to the funds, they are not owned by you (but rather held for you). Therefore, the Trustee can pay the superannuation death benefits as the Trustee determines – which may or may not be in keeping with your wishes.

If you die having a superannuation member interest, the Trustee is obligated to pay the death benefit to any one or more of your “dependents” or your legal personal representative – unless you have made a Binding Death Benefit Nomination (and the Nomination names a lawful payment direction).

You may have significant superannuation death benefits, and have no idea! We discover this quite often, when we ask clients to provide copies of their superannuation statements.

For example, one standard cover by Sunsuper provides a combined total and disability cover for a 30 year old in the sum of $250,000, which decreases at age 60 to $25,000. Also, many industry funds have basic insurance coverage that is taken out on joining the superannuation fund.

In a Will, directions can be made in respect to your wishes on the payment of the superannuation death benefits. The Trustee may have regard to your wishes contained in your Will, but is not bound to act in accordance with your Will. However, your Will is an excellent starting point for the Trustee to consider, in assessing how the superannuation death benefits should be paid. Of course, making and maintaining a valid Binding Death Benefit Nomination in the form required of the Trustee is the best approach to ensuring the benefits are paid to the correct beneficiary.

You do need to be aware, however, that the Trustee is limited to who it can pay – including generally your parents, your children, your partner or spouse and your dependents and interdependents (in general terms – people whom you live with or whom rely on you for some level of financial assistance, or vice versa). Excepting in respect to any one or more of these, the Trustee must pay the death benefit to the Legal Personal Representative of your Estate.

Assuming the death benefits are paid to the Legal Personal Representative of your Estate, if you have no Will – the superannuation death benefit will be distributed in accordance with the intestacy rules set out in your state of residency’s intestacy rules (see, for example, the Succession Act 1981 (Qld)). But, you may not want to leave your death benefit to those who would take intestate, so it pays to draw a Will – regardless of the value you believe your Estate to be worth.

Secondly, if you do not have a Will, there is a question over who controls your Estate.

A properly drawn Will appoints an executor, which person (or people) has the authority to administer your Estate.

In the event that you die without a Will, the only way that a person can be granted authority to deal with your estate (in a way that is recognised by financial institutions and asset holders) is for that person to obtain a grant of Letters of Administration from the Supreme Court.

The cost and time involved in obtaining the grant of Letters of Administration is generally greater than that of obtaining Probate of a Will.

If you would like to speak to our estate planning team about drawing a Will, please contact our office on 07 5574 3560 or via email.